Introduction to Tax Liability

Tax liability is the total amount of tax debt owed to a government by an individual, corporation, or other entity. It is the amount of money that you owe to the IRS or another taxing authority when you finish preparing your tax return.

Your total liability would also include any balances still owed from previous years.

Definition

Tax liability is the payment owed by an individual, business, or other entity to a federal, state, or local tax authority. Generally, you have a tax liability when you earn income or generate profits by selling an investment or other asset. It is possible to have no income tax liability if you don’t meet the income requirements to file taxes.

Different Forms

There are different forms of tax liabilities which include income taxes, sales tax, and capital gains tax. Taxes are imposed by various taxing authorities:

- federal

- state

- and local governments.

In the upcoming sections of this article, we will delve deeper into understanding the calculation of tax liability, how filing status affects tax liability, tax liability for different entity types, effective ways to lower your tax liability, and the importance of accurately calculating your tax liability.

Tax Liability and Filing Status

Your filing status directly affects your tax liability. Your income tax liability is determined by your earnings and filing status.

How Filing Status Affects Tax Liability

Each filing status has its own tax brackets (although married couples filing jointly and qualifying widow(er)s use the same tax table); these represent the rates at which the individual or couple’s income is taxed as they reach certain thresholds.

Different Tax Brackets for Different Filing Statuses

There are different tax brackets for single filers, married couples filing jointly, married couples filing separately, and heads of households. These brackets are adjusted each year for inflation.

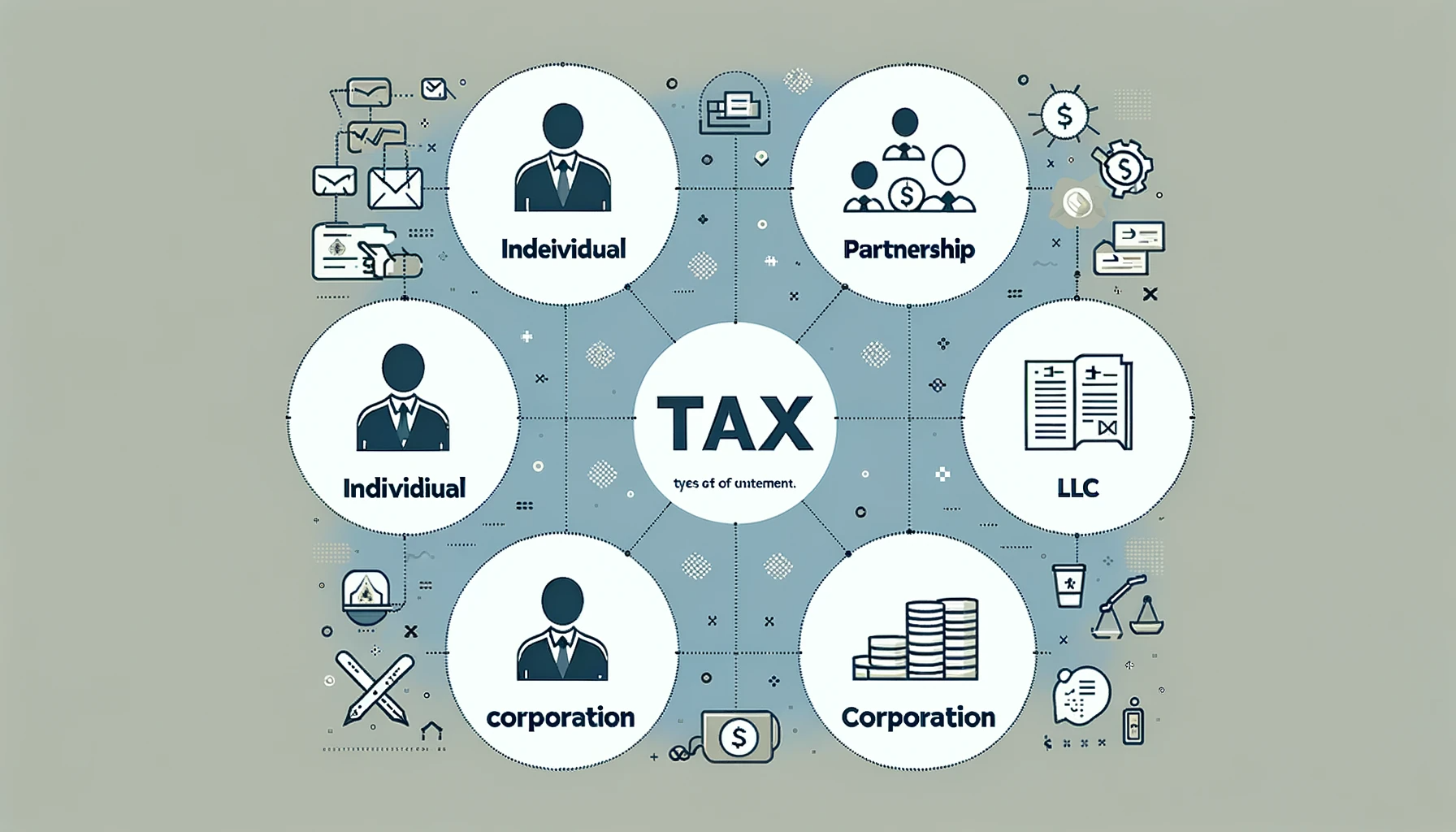

Tax Liability for Different Entity Types

| Entity Type | How Income is Taxed | Personal Liability for Taxes | Notable Tax Characteristics |

|---|---|---|---|

| C Corporation | Corporate tax rate applied to profits; dividends taxed at shareholder’s personal rate | No personal liability; corporation pays taxes | Double taxation on dividends; deductions for business expenses |

| S Corporation | Pass-through taxation; income reported on shareholders’ personal tax returns | Limited personal liability; taxes paid at individual level | Avoids double taxation; salary and dividend income split |

| LLC | Pass-through taxation; income reported on owners’ personal tax returns | Limited personal liability; taxes paid at individual level | Flexible tax structure; can choose to be taxed as C Corp |

| Partnership | Pass-through taxation; income reported on partners’ personal tax returns | General partners personally liable; limited partners not | Must file an informational return; individual partners pay tax |

| Sole Proprietorship | Income reported on owner’s personal tax return | Owner personally liable for taxes | Business losses can offset other income; self-employment tax applies |

Explanation for C corporations

C corporations, also known as C corps, are legally considered separate entities from their owners. They are subject to corporate income tax and their profits are taxed when they are earned. This is the first layer of what is commonly referred to as “double taxation”. If the C corporation distributes dividends from its after-tax profits to its shareholders, these dividends are subject to a second layer of taxation on the shareholders’ personal tax returns.

The tax liability of a C corporation is calculated by applying the corporate tax rate to its taxable income. The taxable income is determined by subtracting business expenses, including operating expenses, cost of goods sold (COGS), and depreciation, from the corporation’s total income.

Understanding of “flow-through” entities

Flow-through entities, also known as pass-through entities, include structures like Sole Proprietorships, Partnerships, LLCs, and S corporations. Unlike C corporations, these entities are not subject to corporate income tax. Instead, the income earned by the business is “passed through” to the owners’ individual tax returns, and tax is paid at the individual income tax rates.

This structure avoids the “double taxation” issue faced by C corporations. However, it also means that the business owners are personally liable for the business’s debts and obligations.

Effective Ways to Lower Your Tax Liability

Strategies to lower taxes owed by claiming deductions, exemptions, and tax credits

There are several strategies that individuals and businesses can use to lower what is owed in tax. These include taking advantage of tax deductions, exemptions, and credits that are available under the tax code.

Tax deductions reduce your taxable income. They can include business expenses for corporations, and for individuals, they can include certain medical expenses, state and local taxes paid, mortgage interest, and charitable contributions, among others.

Tax exemptions also reduce taxable income. While they are less common now for individuals due to changes in the tax code, they are still relevant for certain types of businesses.

Tax credits are perhaps the most powerful tool for reducing tax liability because they provide a dollar-for-dollar reduction in tax. Examples include the Child Tax Credit for individuals and the Research and Development (R&D) Tax Credit for businesses.

Conclusion

The consequences of miscalculating tax liability

Miscalculating what you owe in tax can have serious consequences. If you underpay your taxes, you may be subject to penalties and interest charges by the IRS. In severe cases, it could also lead to criminal charges of tax evasion or fraud.

The importance of consulting with a tax professional or using reliable tax software

Given the complexity of the tax code and the severe consequences of making mistakes, it’s important to consult with a tax professional or use reliable tax software to calculate your tax liability.

A tax professional can provide personalized advice tailored to your specific circumstances. Reliable tax software, on the other hand, can guide you through the process of calculating what is owed, ensuring that you take advantage of all the deductions, exemptions, and credits you are entitled to.

FAQs about Tax Liability

What is Tax Liability?

Tax liability is the total amount of tax owed by an individual, corporation, or other entity to a government authority, such as the IRS or state and local taxing bodies. It encompasses the taxes due on income, investments, sales, and other taxable events.

How Does Filing Status Affect Tax Liability?

Your filing status, such as single, married filing jointly, or head of household, significantly influences your tax liability. Different filing statuses have distinct tax brackets, determining the rate at which your income is taxed.

What are the Different Types of Tax Liabilities?

There are various forms of tax liabilities including income tax, sales tax, and capital gains tax. The specific types of tax liabilities you face depend on factors like your income sources, investments, and purchases.

How is Tax Liability Calculated for C Corporations?

For C corporations, tax liability is calculated by applying the corporate tax rate to their taxable income. This income is determined after subtracting allowable business expenses, such as operating costs and depreciation, from total revenue.

What are Flow-Through Entities and How are They Taxed?

Flow-through entities, like S corporations, LLCs, and partnerships, pass their income directly to the owners’ personal tax returns. They avoid corporate income tax, with owners paying individual tax rates on this income.

What Strategies Can Lower My Tax Liability?

You can lower your tax liability by utilizing deductions, exemptions, and tax credits. Deductions reduce your taxable income, exemptions further decrease it under specific conditions, and tax credits directly reduce the amount of tax owed.

What Happens If I Miscalculate My Tax Liability?

Miscalculating tax liability can lead to underpayment, resulting in penalties and interest charges from the IRS. Severe cases might even lead to criminal charges of tax evasion or fraud.

Why Should I Consult a Tax Professional or Use Tax Software?

Given the complexity of tax laws, consulting a tax professional or using reliable tax software ensures accurate calculation of your tax liability. These resources help in taking full advantage of deductions, exemptions, and credits while avoiding costly errors.